NEW STRATEGIES FOR SCALABLE INNOVATION

Futureproofing Core Banking Systems with Fintech

Inflexible core systems and legacy technology are hurdles to any bank looking to create customer-centric products and journeys. But fintech platforms allow financial institutions to work with their legacy technology instead of around it, clearing the way for new, personalized offers and tailored products.

An Intro to Financial Product Management

Core Banking, Redefined

However, banks still need to keep pace with technology and customer expectations. And while most banks offer online banking, they can be lacking in other areas. Customers expect services like account opening, deposits, and credit processing to be accessible from anywhere on any device – without having to visit their local branch.

These services are integral to core banking systems, but many financial institutions run the risk of falling behind and losing customers if those systems become outdated. With all this in mind, how can banks adapt and keep up?

Raising the Bar for Core Banking

While core banking systems have been instrumental in facilitating this immediacy, they have somewhat reached their limits in terms of supporting banks' product innovation and management processes. This leaves banks somewhat stuck. Deeply entrenched legacy systems are hindering innovation, but the risk and cost associated with completely replacing those systems can put banks years behind their competition and delay all new product launches.

.jpg)

The Pressure Is On for Banks

200 digital banks have launched since 2015 and competition is now coming from within and outside the industry with big tech companies like Amazon and Tesla coming into the financial services space. And while nimble startups and tech giants have the technology and talent to make them agile in responding to customer needs with innovative offers and customer experiences, this is not the case for incumbent banks.

According to a Capgemini report, 40% of customers say their banks currently don’t offer an innovative or personalized experience. In order to compete and avoid losing customers, banks will have to fundamentally rethink the way they define, manage and distribute financial products.

According to a Capgemini report, 40% of customers say their banks currently don’t offer an innovative or personalized experience. In order to compete and avoid losing customers, banks will have to fundamentally rethink the way they define, manage and distribute financial products.

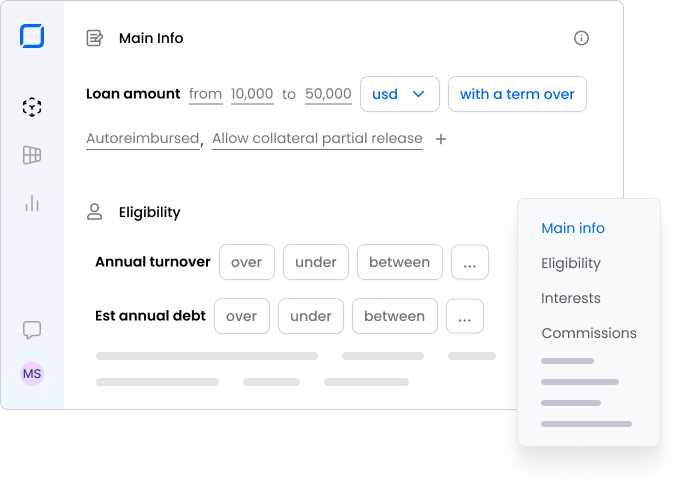

Banks need to break their product management free from core banking platforms and decouple product innovation from outdated and inflexible core systems. This doesn’t mean ripping and replacing existing systems, but instead introducing a flexible product management and launch layer (known as fintech enablement) that integrates with them as well as any other partner products and services the bank might wish to employ. By adding a fintech enablement layer, banks can adapt rapidly to market fluctuations and grow at a pace that suits their requirements.

Rather than relying on costly and costly IT initiatives for every new product introduction or modifications to an existing offer, fintech enablement platforms empower product and proposition managers to define, distribute, and evaluate product performance independently via straightforward no-code tools, digital journey templates, and data dashboards.

Whether banks aspire to create complete end-to-end banking solutions, finely tuned products to cater to specialized customer segments, or simply new offerings based on existing products, fintech enablement can help them transition from a minimum viable product to a live product in mere weeks, not years. This gradual approach enables them to modernize their IT infrastructure with composable capabilities.

Futureproofing Core Banking With Fintech Enablement

Whether banks aspire to create complete end-to-end banking solutions, finely tuned products catering to specialized customer segments, or simply new offerings based on existing products, fintech enablement can help them transition from a minimum viable product to a live product in weeks, not years. This gradual approach enables them to modernize their IT infrastructure with composable capabilities.

No More Ripping and Replacing

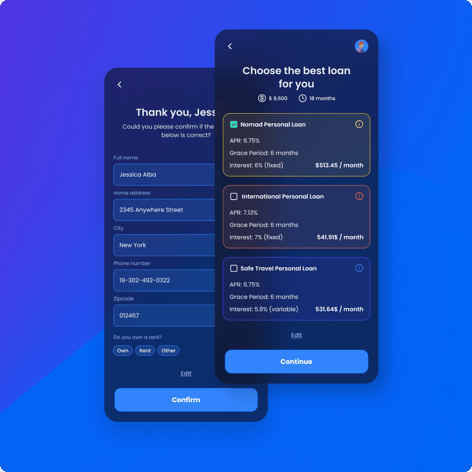

By leveraging fintech enablement platforms, financial product teams can not only independently define and reimagine products and services with speed, but also distribute them to customers and partners through fully digitalized customer journeys. These journeys can be tailored to suit the specific product and channel, whether it's the bank's own website or mobile app, a broker, or an e-commerce partner, ensuring that customers enjoy a seamless experience, regardless of where they choose to make a purchase. This means that banks can reserve IT teams for the most technical tasks, such as complex integrations. Fintech enablement platforms also allow IT teams to modernize their systems gradually and on their own schedule. By decoupling product innovation from rigid systems, banks can replace specific components as needed, leveraging pre-built and composable business capabilities for product definition, journey creation, and servicing. This approach to core modernization, once a risky and time-consuming process costing millions of dollars, is now much easier and safer, with no disruption to daily operations.

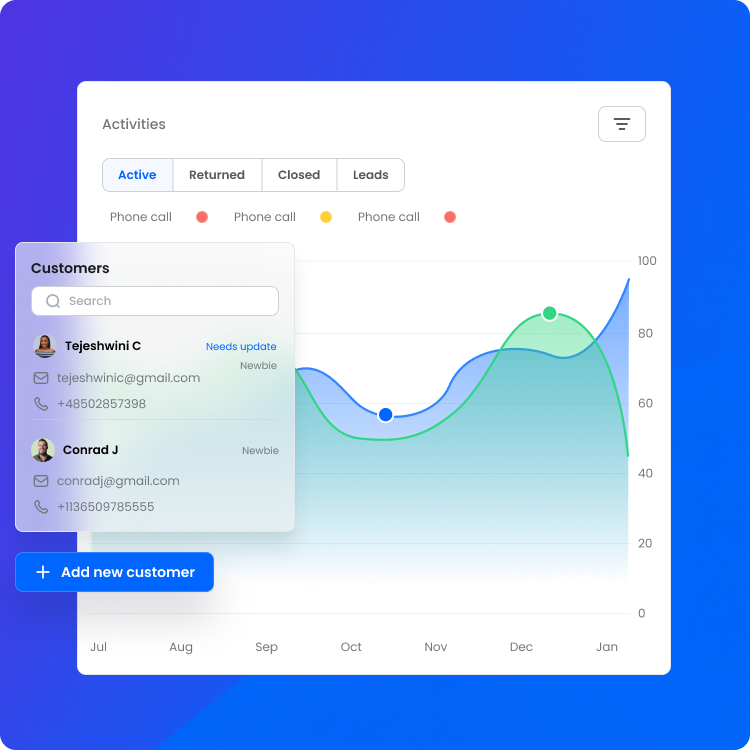

Fintech enablement platforms also allow IT teams to modernize their systems gradually and on their own schedule. By decoupling product innovation from rigid systems, banks can replace specific components as needed, leveraging pre-built and composable business capabilities for product definition, journey creation, and servicing. This approach to core modernization, once a risky and time-consuming process costing millions of dollars, is now much easier and safer, with no disruption to daily operations. One of the greatest benefits of fintech enablement platforms is the ability to integrate the data and capabilities of internal systems with innovative services from the broader fintech ecosystem. This combination provides banks with a powerful set of tools for developing and delivering new products and services to their customers quickly and efficiently.

Fintech enablement platforms offer banks and financial institutions the ability to incorporate cutting-edge technologies into their products and digital journeys, without the need for specialized talent or outside vendors. This is achieved by enriching their existing systems with third-party fintech ecosystem solutions and services. By leveraging these solutions, financial institutions can save time and money, while also staying ahead of the curve in terms of technological innovation.

.png?width=701&height=643&name=shutterstock_2%202%20(1).png)

Fintech Enablement Makes Banking Modernization & Innovation Possible

Fintech enablement platforms offer more than just the ability for business users to innovate on products and customer experiences - they also help IT teams tackle technical debt and modernize their systems.

By decoupling innovation from inflexible systems and offering composable business capabilities, banks can modernize their systems gradually and at their own pace, eliminating the need for costly and risky "rip and replace" approaches for core modernization. This way, banks can prioritize both customer-centric innovation and system modernization without risking disruption to their business operations.